What Awaits Banks in Uzbekistan in the Era of Global Transformations?

The global banking sector is undergoing profound transformation influenced by digitalization, shifting customer expectations, and heightened competition from fintech companies. Banks worldwide are actively reconsidering their strategies concerning product development, service delivery, and customer experience, with a growing emphasis on personalization, technological advancement, and sustainability.

The regional РжгуЃЈLeyuЃЉЬхг§ЙйЭј team, led by Bolat Mynbayev and Khorlan Adilova, has been integrated into the Global Banking Hubтan international expert platform dedicated to the financial services industryтand contributed to the development of the РжгуЃЈLeyuЃЉЬхг§ЙйЭј Global Digital Banking Trends & Insights 2025 report. This research identifies global trends that are becoming increasingly significant for the markets of Central Asia. For Uzbekistan, these trends primarily signify a shift from basic automation processes towards more advanced and sophisticated service models. Rapidly increasing client expectations, fintech influence, an underserved youth segment, and the potential of artificial intelligence collectively define the agenda for sectoral transformation.

Increasing Client Expectations

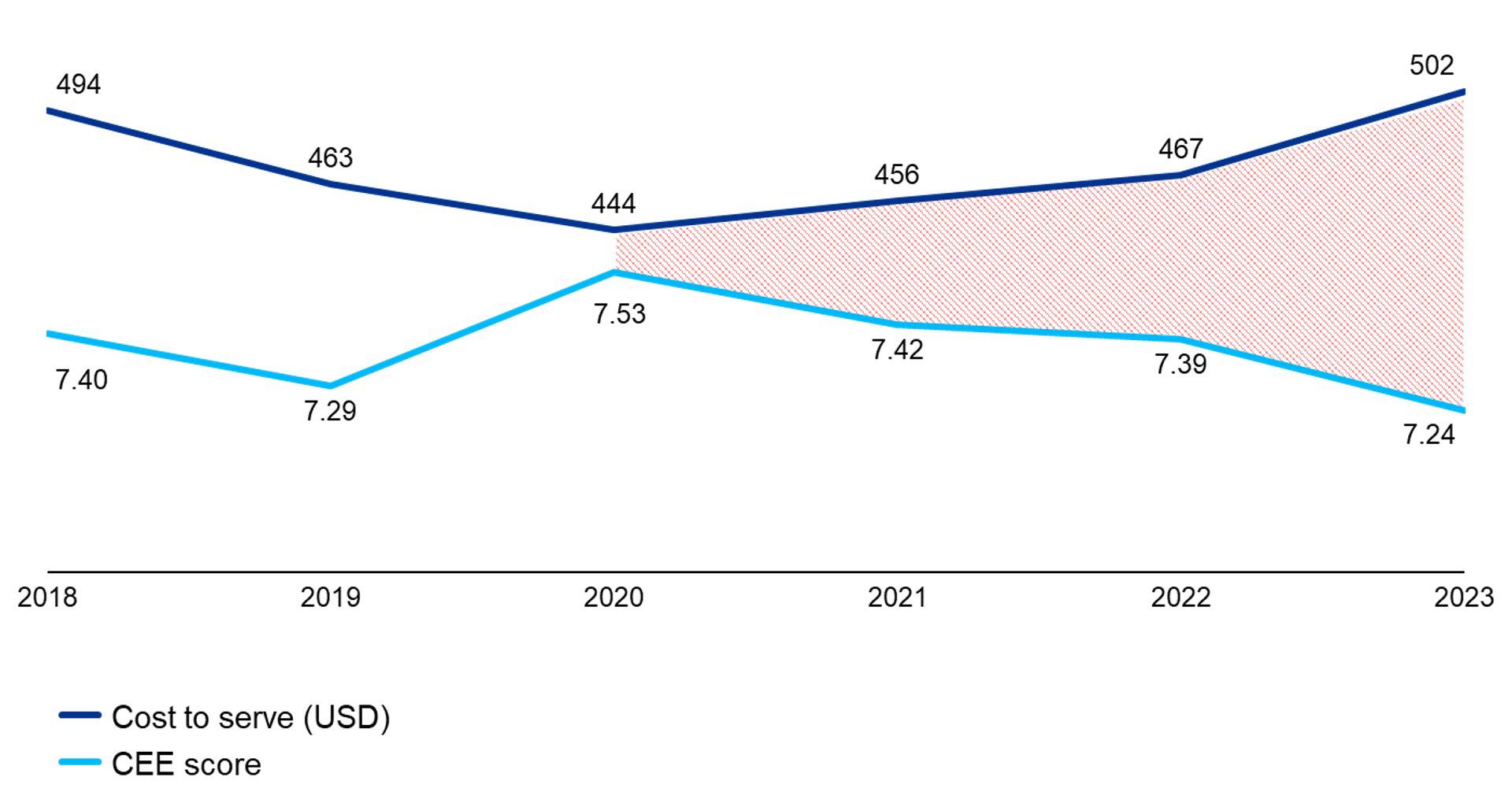

One of the most salient global trends in banking is the escalation of client expectations. According to РжгуЃЈLeyuЃЉЬхг§ЙйЭј, contemporary banking customers anticipate not only efficient and convenient services but also a personalized approach characterized by empathy and transparency. An analysis of data from 2018 to 2023 demonstrates a persistent trend of widening disparity between service costs and the quality of customer experience. Despite increased expenditures, customer experience levels have declined, indicating diminishing returns on investments in client service operations.

In the context of the local market, it is worth noting that banks in Uzbekistan have begun to gradually adapt to rising customer expectations: user interfaces are being updated, support for third-party cards is emerging, and application stability is improving. However, meeting these growing expectations requires a transition from isolated changes to systemic transformation. Personalized service scenarios, developed based on behavioral analytics and continuous feedback, are coming to the forefront. According to the РжгуЃЈLeyuЃЉЬхг§ЙйЭј study, customer satisfaction is shaped at the intersection of six factors: empathy, personalization, time savings, clarity of expectations, accountability for decisions, and adherence to ethical standards.

Customer Care: Beyond Traditional Banking Services

A subsequent key trend in international practice is the gradual move beyond traditional banking servicesтfrom being a transactional intermediary to becoming a platform that supports customers across various aspects of their lives. One international example is Barclaysт� initiative тDigital Wings,т� which provides users access to digital educational content, including videos, articles, and interactive quizzes aimed at enhancing digital literacy and confidence in using online services. Modern banks strive to become comprehensive support hubs, offering not only basic financial services such as transfers and payments but also assistance with educational, social, and life-related issues. Manifestations of this approach range from digital learning services and budgeting assistants to tailored interfaces and personalized interaction scenarios. More advanced models include AI-powered tools that help detect stress and vulnerability and provide flexible support formats depending on clientsт� life circumstances.

This global trend of transforming customer service is also reflected in Uzbekistanтs banking sector, where conditions are gradually being established for a transition to a client-centric model. Fintech companies continue to play a leading role in these changes due to their agility, niche products, and active user engagement. Consumers increasingly expect precise, personalized, and socially meaningful solutions, pushing banks to reconsider their approaches. Moving from fragmented initiatives to a comprehensive model with a clear strategy, unified standards, and regular adaptation of the customer journey becomes an essential condition for meeting these expectations.

Youth Banking: A New Priority for Future Growth

The third significant direction in the transformation of the banking sector is the development of youth bankingтa systematic approach to engaging the young demographic as a source of long-term growth. International experience demonstrates that working with younger audiences is viewed as a strategic investment in future expansion. According to РжгуЃЈLeyuЃЉЬхг§ЙйЭј estimates, by 2030 the aggregate income of individuals under 30 will increase by 400%, reaching $33 trillion, while approximately $84 trillion in wealth will be transferred to young consumers. In response, banks are implementing educational and gamified solutions designed to equip teenagers with fundamental financial skills and facilitate early integration into the banking ecosystem.

This trend holds particular importance for Uzbekistan, where youth under 30 comprise more than half of the population. However, the majority of banks do not currently address this segment in a comprehensive manner. Available solutions remain fragmented and limited to basic functionalities such as cards with spending limits, parental controls, digital lessons, and educational programs. Only a few market playersтno more than four or fiveтoffer products incorporating elements of financial literacy, yet a holistic strategy encompassing the entire customer journey of young clients has yet to be developed. The youth segment remains one of the most promising areas for future growth.

To strengthen their position in this domain, banks must develop a full-fledged product portfolio: adapting user interfaces to different age groups, integrating foundational educational modules, and establishing consistent client support throughout the customer lifecycle. The proposed model will help engage young audiences from an early age, enhance financial literacy, and create a foundation for long-term loyalty.

Artificial Intelligence: The New Architecture of the Banks of the Future

Amid the backdrop of global digital transformation, artificial intelligence (AI) has emerged as one of the key drivers of change within the banking industry. International experience confirms its high efficacy: according to РжгуЃЈLeyuЃЉЬхг§ЙйЭјтs The Intelligent Bank 2025, over 80% of banks regard AI as a strategic asset. Expected benefits include cost reduction, enhanced decision accuracy, and improved customer experience. Countries such as China, the Netherlands, and Sweden have already implemented large-scale AI use cases in underwriting, fraud detection, service automation, and product personalization.

The development of AI holds particular significance for Uzbekistan, as it has been designated a technological priority at the state level. The Presidential Decree titled On ТЋApproval of the Strategy for the Development of Artificial Intelligence Technologies until 2030ТЛ, adopted in April 2024, envisions the establishment of a regulatory framework, development of technical infrastructure for data processing and AI project implementation, execution of priority initiatives in social and economic spheres, as well as enhancement of digital skills among the population and the development of human capital.

According to РжгуЃЈLeyuЃЉЬхг§ЙйЭјтs assessment, the maturity level of Uzbekistani banks in AI adoption remains low. Unlike countries with more advanced digital infrastructure, AI is not yet applied in critical processes such as customer experience management, operational automation, and decision-making. Key barriers include outdated IT systems, weak data integration, and limited human resources in analytics and technology.

Nevertheless, the potential of AI for banks in Uzbekistan is substantial. The rapidly growing volume of digital transactions and high mobile banking activity generate an extensive behavioral data set. This data can be leveraged to build credit scoring models, anti-fraud systems, personalized marketing, and demand forecasting tools. Implementing AI in contact centers, risk management, and credit processes will enable cost reduction, faster service delivery, and greater decision accuracy. Realizing these opportunities will require banks to modernize their IT architectures, deploy data governance systems, and comply with new standards for algorithmic transparency and interpretability.

ааОаНбаАаКбб

Bolat Mynbayev

Partner

Strategy & Operation

РжгуЃЈLeyuЃЉЬхг§ЙйЭј Caucasus and Central Asia

[email protected]

Tel.: +7(771) 800-45-52

Khorlan Adilova

Associate Director

Strategy & Operation

РжгуЃЈLeyuЃЉЬхг§ЙйЭј Caucasus and Central Asia

[email protected]

Tel.: + 7(705) 788-78-51