As a significant step affirming the commitment to implementing electronic invoicing (e-invoicing) in Oman, on 12 May 2025, the Oman Tax Authority (OTA) signed the implementation agreement with their implementation partner.

The OTA intends to implement e-invoicing in a phased manner from Quarter 3 of 2026. With that, Oman is the third country in the Gulf Cooperation Council (GCC) to announce the implementation of e-invoicing. The Kingdom of Saudi Arabia (KSA) implemented e-invoicing in a phased manner from December 2021, and the United Arab Emirates (UAE) has proposed implementation from Quarter 2 of 2026. For the timelines on e-invoicing implementation across the world, you can access our global tracker.

What is an e-invoice?

- An invoice issued in an electronic format, generated through electronic means, and includes the information specified by the OTA.

- It is not merely a digitized form or duplication of a paper invoice or invoice image.

The OTA vide Ministerial Decision No 456/2022 dated 16 October 2022 has already amended the Oman Value Added Tax (VAT) Executive Regulations to introduce provisions on electronic tax invoices, including penalties for non-issuance of electronic tax invoices.

Expected e-invoicing timelines

The OTA intends to implement e-invoicing in a phased manner from Quarter 3 of 2026. The expected e-invoicing timelines for different taxpayers are represented below.

(LTP: Large Taxpayers; B2B: Business-to-Business; B2G: Business-to-Government; B2C: Business-to-Consumer, G2B: Government-to-Business)

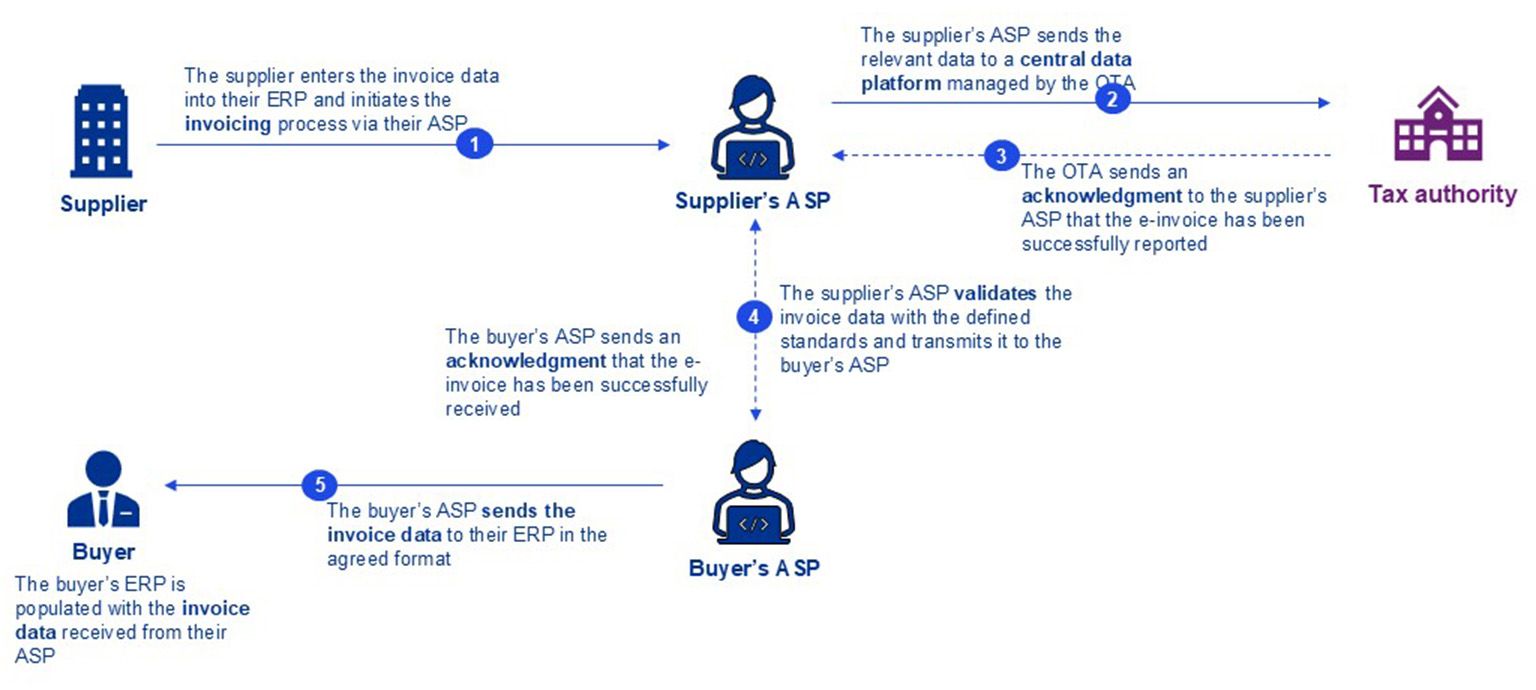

Proposed e-invoicing model

There are different models of e-invoicing and digital reporting adopted by countries across the world. The OTA intends to base e-invoicing in Oman on the Pan-European Public Procurement Online (PEPPOL) 5 corner model that interposes an Accredited Service Provider (ASP) in the document flow, as represented below.

While KSA has implemented the clearance model requiring taxpayers to submit invoice data to the tax authority for approval before issuance, like Oman, the UAE also intends to implement the PEPPOL 5 corner model.

Key considerations for businesses

E-invoicing is likely to impact different facets of business, existing ERP systems and business processes. Among other matters, businesses need to focus on:

- Understanding compliance requirements: Familiarize themselves with the e-invoicing regulations, compliance requirements, data and document requirements.

- System readiness: Evaluate the readiness of the ERP system to ensure availability of adequate data fields and data security/encryption measures along with the ability to integrate with the e-invoicing platform.

- Manual transactions: Identify transactions or documents that are currently not recorded through the ERP system to ensure their coverage for e-invoicing.

- Stakeholder and change management: Educate stakeholders likely to be impacted (including but not limited to tax, finance, IT, accounts receivable, accounts payable and legal), and proactively engage in stakeholders and change management clearly defining and communicating roles and responsibilities, timelines, developments, etc.

- Selecting the right ASP: Identify an e-invoicing ASP to ensure seamless integration with the ERP system and adequate post-integration support and maintenance.

How can 乐鱼(Leyu)体育官网 assist your organization?

While the detailed guidelines/data dictionary from the OTA providing clarity on data fields to be reported, transactions covered, validation mechanism, etc. and the accreditation process for e-invoicing ASP are awaited, businesses can start assessing their readiness based on the guidelines published in comparable jurisdictions using the PEPPOL 5 corner model.

We, at 乐鱼(Leyu)体育官网 Oman, can support you in your e-invoicing journey. We can assist you in preparing for the current situation and advise on the next steps including the following:

- Business process mapping: Conduct stakeholder workshops to map technology, data, VAT compliance risks, business transaction flows, scenarios and assess the likely reportability/updates required for e-invoicing.

- Impact assessment and gap analysis: Review existing systems, processes and transactions to identify potential changes and/ or updates required in the ERP system or business processes.

- Change management and training: Assist with the change management strategy including stakeholder awareness sessions through bespoke training sessions.

- Implementation roadmap and support: Assist with drafting the implementation roadmap for system readiness and implementation support.

- Vendor selection: Assist with the e-invoicing ASP selection.

乐鱼(Leyu)体育官网 has a dedicated team of experienced indirect tax specialists based in Oman, supported by a larger, experienced regional team. The team has hands-on experience of implementing e-invoicing in other jurisdictions. If you need assistance with e-invoicing or other indirect tax related matters, please reach out to your advisors at 乐鱼(Leyu)体育官网 or the contacts mentioned below.