The Maltese regulatory framework provides for different types of entities including public companies, partnerships en commandite (鈥渢he limited partnerships鈥�), or partnerships en nom collectif (鈥渢he general partnerships鈥�), an association en participation, a Societas Europaea (the 鈥淓uropean Company鈥�), a European Economic Interest Group (鈥淓EIG鈥�), and the most popular being the private limited liability company.

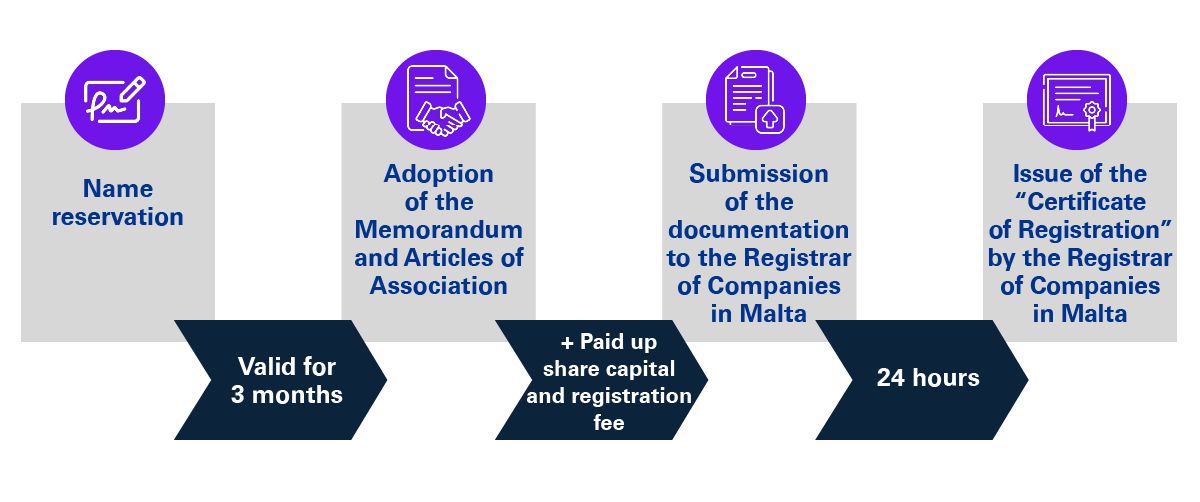

Registration of public and private companies in Malta is a relatively quick process. It is normal for the registration of the company to be completed by the issue of a 鈥淐ertificate of Incorporation鈥� by the Registrar within 24 hours of all the requisite documentation being submitted electronically to the Malta Business Registry.

Documentation required for incorporation

One of the essential documents required for the incorporation of a Maltese company is the Memorandum of Association, which includes key information such as the company name, the objects, the share capital, the subscribers, the company directors, and information relating to the company secretary.

There is also the need to submit the Articles of Association of the company which document regulates the internal management of the company. The contents of the Memorandum and Articles of Association may vary depending on the type of company, for example, the Memorandum and Articles of Association of a private limited liability company must restrict the transfer of its shares, limit the number of members to 50, and prohibit any invitation to the public from subscribing to any shares or debentures of the company.

It is worth noting that a Maltese company may be set up with only one shareholder, and such single member company in its Memorandum or Articles of Association, must:

- determine which activity is to be its principal activity;

- limit the number of persons holding debentures of the company to not more than 50;

- prohibit any body corporate from being a director of a company and;

- prohibit the company and each of the directors from being a party to an arrangement whereby the policy of the company is capable of being determined by persons other than the directors, members, or debenture holders thereof.

Few additional requirements exist for public companies and special vehicles such as SICAVs.

The Registrar must also be provided with the evidence that the subscribed share capital has been paid up, such as a bank deposit slip, and documentation relating to the subscribers and the directors of the company.

Company Names

Upon deciding on a company name, a name reservation that is valid for three months shall be obtained. In general, every name requires the approval of the Registrar, who has the power to refuse registration in certain cases, e.g. if the name is offensive. The name of a private company must end with the words 鈥榩rivate limited company鈥�, 鈥榣imited鈥�, or the abbreviation 鈥榣td鈥�, while that of a public company must end with the words 鈥榩ublic limited company鈥� or the abbreviation 鈥榩lc鈥�.

Minimum Capital

The minimum authorised capital for a private company in Malta is 鈧�1,164.69 and that of a public company - 鈧�46,587.47. In case of a public company, at least 25% of the issued share capital, and in case of a private company, at least 20% of the issued share capital must be paid-up on the signing of the Memorandum of Association of the company.

Shareholders

The number of shareholders in a Maltese company differs on the type of company. A single member private limited company has a minimum of one shareholder, whilst a minimum of two shareholders is set for private companies and public companies. A maximum number of 50 shareholders is set for a private limited liability company.

It is worth noting that there are no legal requirements with respect to nationality or residency of a shareholder of a company under Maltese law, and both nominee shareholding and holding of shares under trust are permitted.

Company director and secretary (Management)

The Memorandum of Association must appoint the first director (being either a natural or a legal person) of the company, being a minimum of one with respect to private limited liability companies, and two in the case of public companies.

A Maltese company is managed by its directors who have the authority to execute all the powers of the company, apart from matters reserved to the shareholders in terms of the Companies Act, or reserved matters in terms of the company鈥檚 constitutive documents. In addition, the Memorandum of Association must also indicate the first company secretary, who must be an individual. The role of the company secretary is that of an administrative officer, carrying with it functions and responsibilities at law.

Following incorporation, a Maltese company will have certain minimum obligations to adhere to, including the keeping of the registers of members and directors, filing an annual return to the Registrar, and the filing of audited financial statements. In the case of late submissions, the company may incur penalties.

Fees

The registration fee payable to the Malta Business Registry depends on the authorised share capital of the company. The fee starts at 鈧�100, with the maximum set at 鈧�1,900 if the authorised share capital exceeds the total of 鈧�2,500,000. There is also a yearly fee payable to the Malta Business Registry, calculated on the authorised share capital of the company, with the minimum being 鈧�85, and the maximum set at 鈧�1,200 per annum.

Taxation of limited liability companies in Malta

Companies incorporated in Malta are both domiciled and resident in Malta, irrespective of whether the management and control of the company is exercised in Malta or outside. Companies in Malta are subject to a standard tax rate of 35% on their worldwide income, and may claim relief by way of a tax credit, of foreign taxes paid on such income against the applicable Maltese taxes.

Upon a distribution of the taxed profits by a Maltese company to its shareholder/s, the latter may be entitled to claim a shareholder鈥檚 partial tax refund, reducing the effective tax rate to between nil and 6.25%. The amount of refund available depends on the nature of income earned by the Maltese company and on whether the Maltese company has claimed any relief for foreign taxes paid, although typically the refund available is that of 6/7ths of the Maltese tax charge, before the deduction of any credit for foreign taxes, limited to the amount of Malta tax paid.

A full 100% tax refund can be claimed by a Maltese holding company, which derives its profits/gains from a participating holding, provided that it satisfies certain conditions set out in the law.

Entity formation services are provided by 乐鱼(Leyu)体育官网 Advisory Services Limited (C2435). 乐鱼(Leyu)体育官网 Advisory Services Limited is a Maltese limited liability company authorised to act as a Class A CSP by the MFSA.