Can the Values Derived from Purchase Price Allocations Serve as Reliable Comparables?

In the context of corporate acquisitions, companies are typically required to prepare a Purchase Price Allocation (PPA). The PPA allocates the total consideration paid for the acquired business to its identifiable assets and liabilities based on their fair market values at the acquisition date. While the PPA serves accounting purposes, it often includes valuations of intangible assets, which raises an important question: Can a PPA be used as a reliable basis for determining arm鈥檚 length prices in subsequent intercompany transactions?

Transfer Pricing Methods for Transfers of Intangible Assets: CUP vs. HALA

When determining the appropriate transfer price for intercompany transactions, the selection of the most appropriate method is crucial. From the German transfer pricing perspective, two methods are particularly relevant in the context of asset transfers: the Comparable Uncontrolled Price (CUP) method and the Hypothetical Arm鈥檚 Length Approach (HALA).

The CUP method is generally preferred when a comparable transaction between independent parties can be identified. It involves comparing the price charged in the controlled transaction to the price charged in a similar transaction under comparable circumstances. If a reliable CUP is available, it provides a strong and direct indication of an arm鈥檚 length price and is to be preferred to the HALA.

However, in many cases 鈥� especially those involving unique or highly specialized intangible assets 鈥� reliable external comparables do not exist. In such situations, from a German perspective, the application of HALA is necessary. This approach constructs a theoretical arm鈥檚 length price by simulating the conditions under which independent parties would negotiate a transaction. It relies on economic valuation techniques and requires careful consideration of the functions performed, assets used, and risks assumed by each party.

PPA as Potential CUP

From the OECD perspective, valuations of intangibles contained in PPAs are not determinative for transfer pricing purposes and should be utilized in a transfer pricing analysis with caution and careful consideration of the underlying assumptions.1 From the practical perspective, the question of whether the values derived from the PPA can serve as a CUP in a transfer pricing context is nuanced. A PPA is designed to allocate the total purchase consideration of a business acquisition to the identifiable assets and liabilities based on their fair values. While this process often involves detailed valuations of individual intangible assets 鈥� such as trademarks, patents, and technology 鈥� its primary objective is financial reporting, not transfer pricing compliance. For sound accounting purposes, some valuation assumptions may reflect conservative assumptions and estimates of the value of assets reflected in a company鈥檚 balance sheet. This can lead to definitions that are too narrow for transfer pricing purposes and valuation approaches that are not necessarily consistent with the arm鈥檚 length principle.2

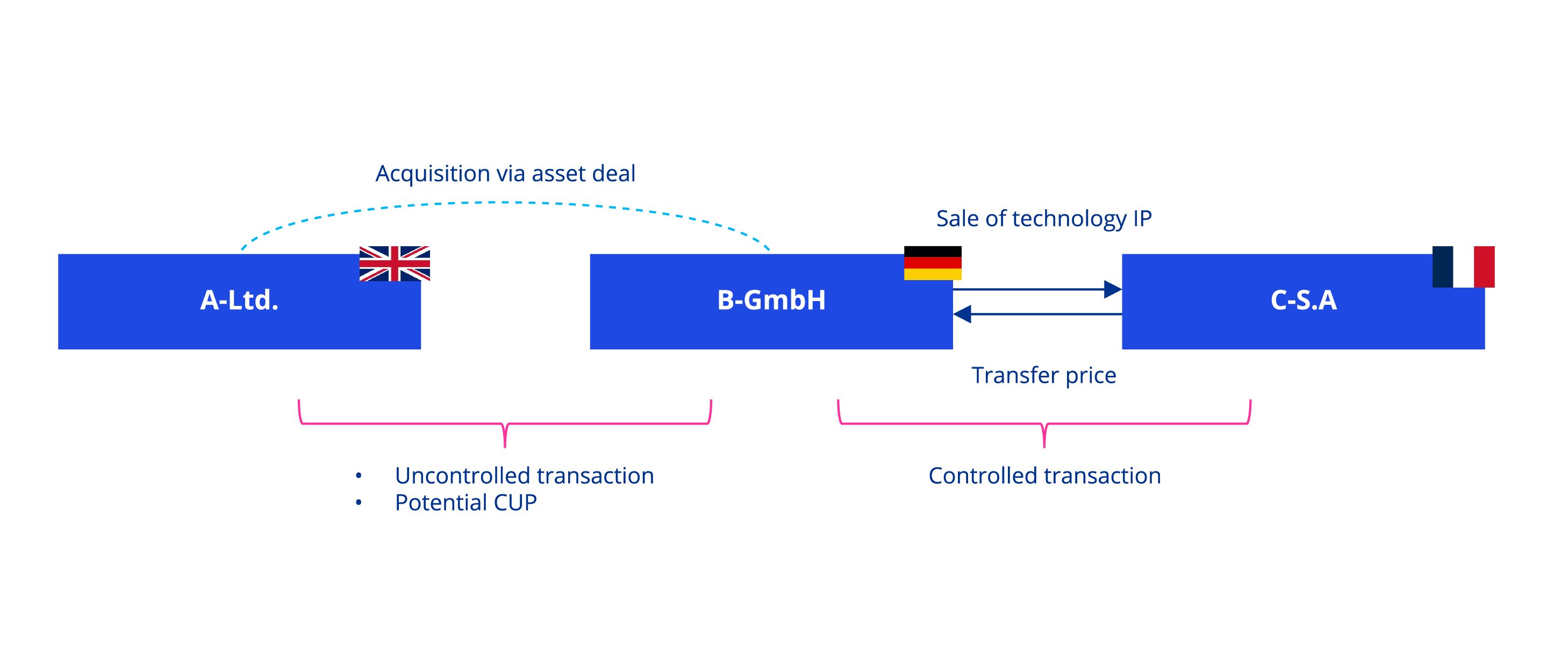

Nevertheless, under certain conditions, a PPA may provide a useful reference point for establishing an arm鈥檚 length price. For a PPA to qualify as a CUP for an intercompany transaction, the following conditions need to be cumulatively fulfilled: i) the intercompany transaction shall be realized without significant time lag, ii) there must be no material differences in the functional and risk profiles of the parties involved compared to those in the controlled transaction. If these criteria are met, the values from the PPA may offer a reliable benchmark.

Still, it needs to be considered that transfer pricing requires a more granular review of the valuation parameters and assumptions used in the PPA. For example, if the relief-from-royalty method was applied to determine the value of intellectual property, the implied royalty rate must be consistent with rates observed in comparable third-party licensing agreements. This typically necessitates a benchmarking analysis to confirm that the royalty rate is at arm鈥檚 length.

In practice, it is common for differences to exist between the controlled and uncontrolled transactions. These differences may relate to the functions performed, the assets employed, or the risks assumed by the parties. In such cases, adjustments to the PPA-derived values may be necessary. For instance, a company-specific Weighted Average Cost of Capital (WACC) used in the PPA might need to be adjusted to reflect market conditions. Other valuation inputs 鈥� such as growth rates, discount rates, or useful lives 鈥� should also be reviewed to ensure they are appropriate from a transfer pricing perspective.

The use of PPA as a CUP is illustrated in the figure below:

When the Hypothetical Arm鈥檚 Length Approach Applies

If the differences between the controlled and uncontrolled transactions are too significant to be addressed through reasonable adjustments, the PPA cannot be used as a CUP. In such cases, the HALA has to be applied under the German transfer pricing rules.

The application of HALA simulates the negotiation process between independent parties. This approach requires a detailed economic analysis of the transaction, taking into account the perspectives of both the buyer and the seller. It is particularly useful when dealing with unique or highly valuable intangible assets for which no reliable market comparables exist.

Even when HALA is applied, certain parameters from the original PPA may still be relevant 鈥� provided they are not affected by changes in the functional and risk profile. For example, the useful life of an intangible asset, such as a patent or software, may remain a valid input in the HALA model if it reflects the asset鈥檚 actual economic utility. Using consistent assumptions where appropriate can enhance the credibility and coherence of the valuation. In addition, useful insights might be gained by revisiting estimates and assumptions that had been used in the original negotiation by the related party buyer, i. e. B-GmbH in the example illustrated above.

Conceptually, HALA can be visualized as a two-sided valuation model. On one side is the minimum price the seller would accept, and on the other is the maximum price the buyer would be willing to pay. The arm鈥檚 length price lies within this range, representing the point at which both parties would agree to transact. The following figure illustrates the calculation of the range of negotiation values.

Conclusion

In conclusion, while a PPA is not designed for transfer pricing purposes, it can, under the right conditions, serve as a useful reference point 鈥� potentially even as a CUP. However, this requires a careful assessment of the comparability of the transactions and the reliability of the valuation inputs. Where significant differences exist, or where adjustments cannot adequately bridge the gap, the HALA has to be applied from the German transfer pricing perspective.

Ultimately, the key to a defensible transfer pricing position lies in a thorough analysis of the facts and circumstances, supported by consistent and well-documented valuation methodologies. By understanding the interplay between PPAs, CUPs, and HALA, taxpayers can better navigate the complexities of cross-border asset transfers and ensure compliance with the arm鈥檚 length principle.

Our 乐鱼(Leyu)体育官网 Transfer Pricing Experts would be pleased to assist you with any questions you may have.

Publication Date:

30 May 2025

1 See Paragraph 6.155, OECD Transfer Pricing Guideline 2022.

2 See Paragraph 6.155, OECD Transfer Pricing Guideline 2022.