The Inland Revenue (Amendment) (Minimum Tax for Multinational Enterprise Groups) Bill 2024 (the Bill)1, together with over 100 government proposed amendments2 to the Bill, were passed by the Legislative Council on 28 May 2025. For more detailed discussions of the Bill and the amendments, please refer to our Hong Kong BEPS publication issued in December 2024 and Hong Kong BEPS publication issued in April 2025.

It is expected that the corresponding Ordinance will be gazetted on 6 June 2025 and become effective on the same date. Upon gazettal of the Ordinance, the Income Inclusion Rule (IIR) and Hong Kong Minimum Top-up Tax (HKMTT) will take effect retrospectively in the Hong Kong SAR (Hong Kong) for fiscal years beginning on or after 1 January 2025 whereas the Undertaxed Profits Rule will become effective from a date to be specified by the government at a later stage.

With the introduction of the global and domestic minimum top-up taxes, the Hong Kong tax system has ushered in a new era for large multinational enterprise (MNE) groups. This publication discusses key considerations and immediate actions that large MNE groups should address following the enactment of the Pillar 2 legislation in Hong Kong.

Implications for 2025 interim financial reporting

The publication of the final legislation on the IIR and HKMTT in the Gazette signifies the enactment of the IIR and HKMTT in Hong Kong, and that is expected to take place on 6 June 2025. For in-scope MNE groups with December financial year end, this means that they will need to deal with the current tax provisions/disclosures in respect of the IIR in Hong Kong and the HKMTT in their interim financial statements for financial year 2025.

As part of the Hong Kong Pillar 2 tax provision exercise, in-scope MNE groups need to obtain the relevant financial and tax data of the in-scope local and/or foreign entities in their groups to perform the following safe harbour assessments:

- provision for top-up taxes under the HKMTT regime (applicable to groups with one or more constituent entity (CE) located in Hong Kong) - the groups need to assess whether they are eligible for the transitional Country-by-Country Reporting safe harbour (CbCR TSH) in respect of Hong Kong,

- provision for top-up taxes under the IIR in Hong Kong (applicable to Hong Kong-headquartered groups only) - the groups need to assess whether they are eligible for the CbCR TSH in respect of the foreign jurisdictions in which they operate and/or whether the QDMTT safe harbour (QDMTT SH) applies in respect of those jurisdictions, and

- provision for top-up taxes under the IIR in the overseas ultimate parent entity (UPE) jurisdiction (applicable to foreign-headquartered groups only) - the groups need to assess whether they are eligible for the CbCR TSH in respect of Hong Kong and/or whether the QDMTT SH applies in respect of Hong Kong.

Given the complexity of the GloBE rules and the rules governing the operation of the CbCR TSH (e.g. the requirement on consistent use of data and the anti-avoidance rules for hybrid arbitrage arrangements) and the QDMTT SH (e.g. the definition of local financial accounting standard and the application of the Switch-off Rule to certain entities), in-scope MNE groups should allocate sufficient time and resources for preparing the Pillar 2 tax provision.

Other key considerations

1. Timeline for Pillar 2 reporting obligations

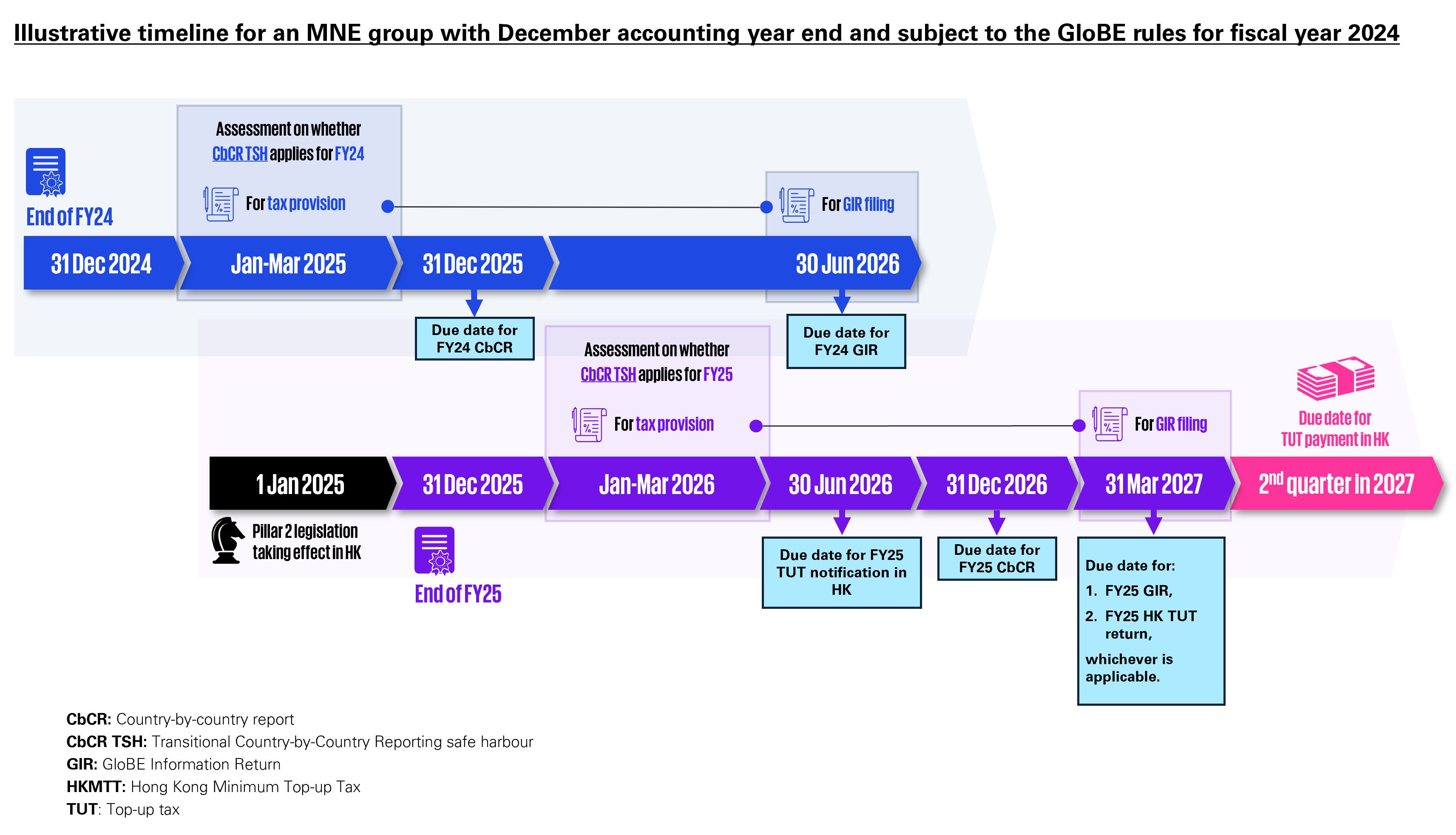

In-scope MNE groups should plan ahead for the additional compliance burden relating to Pillar 2 reporting obligations going forward. We set out in the Appendix a Pillar 2 compliance timeline for an MNE group that is with a December accounting year end and that has been subject to the GloBE rules for the fiscal year ended 31 December 2024 for illustrative purposes.

2. Uncertain areas requiring special considerations

Currently, uncertainties exist as to the interpretation and application of the various aspects of the GloBE rules. Below are a few examples where special attention is required:

- Determination of ownership interests 每 There are various situations where the Pillar 2 rules require a determination of the ownership interests in a particular CE to ascertain the correct treatment that should apply under Pillar 2 (e.g. (1) whether a CE is regarded as Partially-Owned Parent Entity or a Minority-Owned Constituent Entity and (2) whether an equity investment is regarded as Portfolio Shareholding). Other than the issue of data readiness, determining the ownership interests in a CE for Pillar 2 purposes could be particularly challenging when (1) there is a change in the ownership interests in the CE during the fiscal year concerned or (2) different classes of shares (e.g. ordinary shares and preference shares) are issued by the CE which carry different rights in the profits, capital, reserves or voting rights of the CE.

- Special treatments of joint venture (JV) entities 每 Various special treatments apply to a JV and a JV group (i.e. a JV and its subsidiaries) under the GloBE rules. For example, although a JV and its subsidiaries held by an in-scope MNE group are not CEs of the MNE group (as they are not consolidated into the group), a separate effective tax rate computation is required for the JV group to ascertain any amount of top-up tax arising from the JV group for which the MNE group is liable. The fact that a JV entity is not a CE as defined gives rise to considerable uncertainties as to the application of the GloBE rules in various aspects 每 e.g. (1) whether the arm*s length principle under Article 3.2.3 of the GloBE rules applies to transactions between JV entities and CEs located in different jurisdictions and (2) whether cross-border taxes (e.g. dividend withholding taxes and CFC taxes) booked in the financial accounts of a CE of an MNE group (i.e. the JV partner) should be allocated from the CE to the JV under Article 4.3.2.

- A change to fair value accounting for assets 每 While one interpretation of the OECD*s commentary to Article 9.1.3 of the GloBE rules is that step-up of the carrying value of an asset to its fair value for Pillar 2 purposes is not allowed when an MNE group changed it accounting policy after 30 November 2021 to account for its assets at fair value instead of at cost, the Administration*s responses as set out in a report of the Bills Committee3 seem to suggest that an MNE group that is firstly subject to the GloBE rules in fiscal year 2025 may change to fair value accounting for its capital assets (e.g. long-term held immovable property) in fiscal year 2024 so as to step up the carrying value of the assets to their fair values as on the first day of fiscal year 2025 for Pillar 2 purposes. Further clarification from the Administration on whether its above position is agreeable to the OECD would be much welcomed.

- Migration of group entities - With the company re-domiciliation regime in Hong Kong taking effect from 23 May 20254, in-scope MNE groups may consider whether it is beneficial for them to redomicile certain offshore group entities to Hong Kong to make them become a CE located in Hong Kong for Pillar 2 purposes. However, they should take into consideration that (1) an entity which has changed its location during a fiscal year will be regarded as located in the jurisdiction where it was located at the beginning of that year for Pillar 2 purposes and (2) given that the tax carrying values of certain assets of the re-domiciled company may need to be adjusted (e.g. marked down to the fair value as at the date of re-domiciliation) upon re-domiciling to Hong Kong, considerations should be given to whether an election under Article 6.3.4 of the GloBE rules should be made and whether the GloBE deferred tax amount will be different from the accounting deferred tax amount as a result of such election.

The next step

As the next step, we look forward to the timely issuance of the IRD*s local guidance on the interpretation and application of the Pillar 2 rules in various uncertain areas (including the issues highlighted above) to provide greater clarity and certainty for in-scope MNE groups from the Hong Kong domestic compliance perspective. In addition, early release of the Hong Kong top-up tax return that is required to be filed from fiscal year 2025 onwards would facilitate in-scope MNE groups* preparation for Pillar 2 tax filing in Hong Kong.

Appendix

1The Bill can be accessed via this link:

2A complete list of amendments can be accessed via this link:

3The Bills Committee report can be accessed via this link:

4For more details of the company re-domiciliation regime in Hong Kong, please refer to our Hong Kong Tax Alert, Issue 2, May 2025.

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ 氈赶ㄗLeyuㄘ极郤夥厙 kpmg.socialMedia